Written by John Carbrey.

My understanding of how to generate financial wealth changed quickly and fundamentally after I sold my first company.

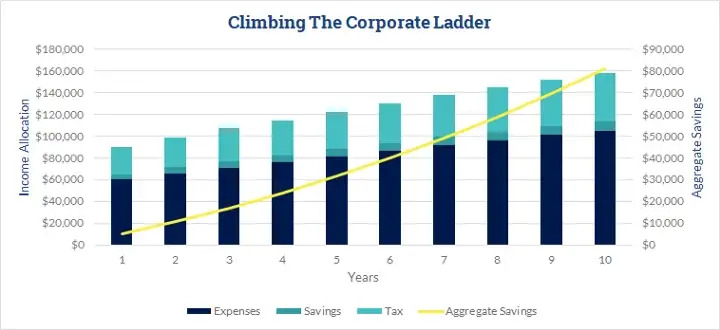

I joined the buyer, a corporation with tens of thousands of employees and billions in revenue, as an SVP. Near the end of my earn-out (I had committed to staying with them for three years), it dawned on me that even public company C-level executives, some of whom were responsible for thousands of employees and hundreds of millions in revenue, had generated less wealth than the founders of our 100-person startup when comparing our earnings from the sale with the combined value of their annual salaries (much higher than ours) and stock incentives.

These executives were in the top 1% of non-founder North American executives in terms of financial wealth. The average North American executive was earning far less. There was certainly money to be made climbing the corporate ladder, I thought, but the reality didn’t line up with the perception. The world’s most wealthy people aren’t necessarily the most senior, and when they are, their seniority is rarely the source of their wealth.

(Before I go on, I want to make a few things clear. First, before thinking about your goals for financial wealth, it’s imperative that you examine the meaning and impact behind your work. Pursuing wealth for the wrong reasons can be hollow, and even tragic. You can read more on my personal experience with this in From Striving to Calling. Second, though it might sound like I’m disparaging these executives, I admire all of them. Their authentic leadership inspired me, and I grew and learned under their coaching and mentorship. I’m using this narrative only to illustrate the shift in my perspective of financial wealth generation, and to dispel the myth of its correlation to one’s position on the corporate ladder.)

Another thing that struck me amid this significant shift in perspective was that most executives appeared, unsurprisingly, to spend more as their salaries increased, resulting in only marginal growth in their financial wealth year over year. Alas, wealth is actually what you don’t spend.

The Five Tenets of the Barbell Strategy

The strategy employed by most of the people I’ve seen generate significant financial wealth was much different. Almost all of them did so not by following this corporate ladder model of pursuing more seniority, prestigious titles, and higher annual salaries, but by following the barbell strategy, which holds these core beliefs:

1) Long-term thinking above short-term thinking. For Barbell Strategy followers, a bird in the hand is not worth two in the bush. They prioritize deferred gains resulting in long-term financial independence over immediate gains that lead to a short-term payday.

2) Forced frugality above instant gratification. A rejection, or at least suspension, of the consumerist mindset — which dictates that the more money you earn, the more you should spend — might be the most difficult Barbell Strategy shift. It’s the marshmallow test for grownups.

3) Upside maximization above downside minimization. Overcoming loss aversion and understanding the asymmetric risk involved in high-growth investments. You will never lose more than 1x what you invested, but you could potentially gain 30x.

4) Regret minimization above fear. This comes from Jeff Bezos’ regret minimization mental model for difficult decisions, which requires you to ask yourself: “In x years, will I regret not doing this?” In the Barbell context, it’s related specifically to your high-growth asset (more below). It was most recently articulated in Bezos’ statement to Congress last summer. “Most of our regrets are acts of omission — the things we didn’t try, the paths untraveled,” he said. “Those are the things that haunt us.”

5) Low and high risk above medium risk. Medium-risk ventures, including employment, can be loaded with hidden risks. Owning part of a customer revenue stream is better than being an employee of the same company.

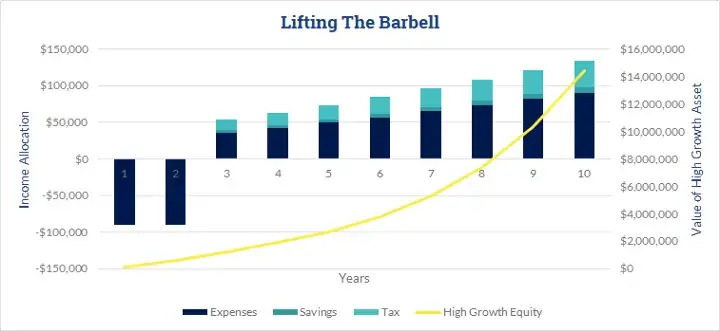

Lifting The Barbell

Instead of investing my time in climbing to the next rung on the Corporate Ladder, whether through an MBA or no-holds-barred competition with peers, and getting a status and lifestyle upgrade, I unknowingly chose, or in a way forced myself, to live modestly. I invested my time and any excess capital into the growth of a company that had the potential to make me financially independent for the rest of my life. In hindsight, I was following in the footsteps of many of my friends and mentors in the tech industry.

As an example of the self-restraint required, I’ve seen a number of those friends and peers build 200-plus-person companies while keeping a salary lower than their mid-level employees for the benefit of the business. On exit, they earned tens of millions of dollars.

(Another caveat: This strategy isn’t practical or even feasible for everyone. As we outlined in The entrepreneurial risk profile, this transition requires a sufficient level of risk capacity and risk appetite.)

I’m looking at this strategy through the lens of entrepreneurship and early-stage venture investing, but it can be more broadly viewed as an approach to resource allocation.

The Barbell’s Origins

I was introduced to the Barbell Strategy by Stuart E. Lucas, an investment professional and one of the heirs to the Carnation Company fortune. I recently attended a private wealth management program he led at the University of Chicago’s Booth School of Business.

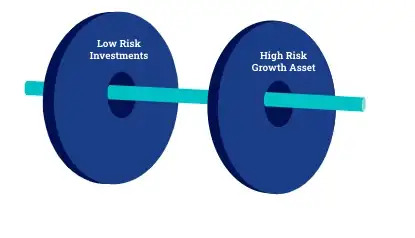

In his book Wealth: Grow It, Protect It, Spend It, and Share It, Lucas presented the model of investing assets in low-risk investments and in “growth assets.” Initially, most of the investment is in high-growth assets, but eventually, the goal is to balance it out with 80 percent in low-risk investments, such as index funds, and 20 percent in growth assets. Wealth is created in growth assets and maintained in the indexed funds. This is how, over time, you can “balance the barbell.” For Lucas, there are three “Critical Success Factors” in this strategy:

In his book Wealth: Grow It, Protect It, Spend It, and Share It, Lucas presented the model of investing assets in low-risk investments and in “growth assets.” Initially, most of the investment is in high-growth assets, but eventually, the goal is to balance it out with 80 percent in low-risk investments, such as index funds, and 20 percent in growth assets. Wealth is created in growth assets and maintained in the indexed funds. This is how, over time, you can “balance the barbell.” For Lucas, there are three “Critical Success Factors” in this strategy:

Contrasting The Two Approaches

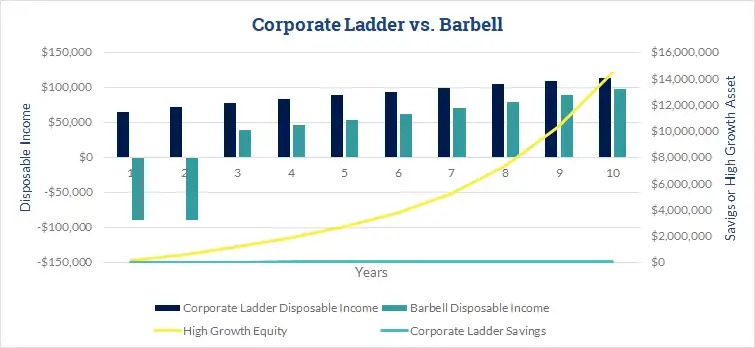

I’ve generated almost all of my wealth by investing the majority of my capital into riskier technology ventures with exponential growth potential and the rest into reasonably safe assets (like ETFs). I make little to no medium-risk investments, and my salary has always been below market value. (I believe you should actually avoid high salaries, as they often signify a lack of equity.)

You might be thinking that the barbell results only materialize in the event that your high-risk investments pan out. To be clear, this article isn’t a call to rush out and start the first business you can think of or invest in any early-stage venture that comes to mind. Lots of work is required to validate a venture’s potential. The key to selecting the right growth asset, according to Lucas, is to “take advantage of your skills, experience, judgment, personal contacts, and professional network to identify attractive opportunities to pursue.” (Wealth, P. 173)

Also, while the barbell strategy line in the graph above isn’t a worst-case scenario, it also isn’t the best-case scenario. Many of my founder peers have seen a 10x, 20x or even 50x return on their time and capital investments.

The corporate ladder line, however, might be the best-case scenario. The possibility of losing a highly coveted job might feel unlikely, but it’s becoming more real in the COVID era. No position is immune, and often the C-suite is at an increased risk due to public accountability and high cost. All but a small executive leadership group in companies are fully aware of the risks.

As noted above, there is plenty of success to be had in climbing the corporate ladder. But it isn’t the only way, or even the best way, to build wealth. The barbell approach provides another framework, but it requires a radically different mindset.

Applying the Barbell Strategy To Your Life

The Barbell Strategy can also be an instructive lens through which to view your career if your goal is financial independence, having skin in the game, or exponentially multiplying your impact.

If your goal is to be comfortable and have a consistently lavish lifestyle without taking on any risk, it likely isn’t for you. I’ve benefited enormously from this path, but it certainly wasn’t always comfortable or glamorous. It has required sacrifice and discipline, both from me and my family.

Aside from the financial independence gained, I can guarantee that walking this unconventional path will show you what you’re made of. If you approach it carefully and thoughtfully, I promise the reward in many areas of your life can be significant, especially if you’re driven by a calling.

Written in collaboration with Stephen Baldwin.

I’m looking to co-create world-class software companies with driven entrepreneurial leaders. Learn more about how as a venture studio we can co-create with you at futuresight.ventures.